Swerve out of car FBT record keeping roadblocks

31st of March every year marks the time to read the car odometer; not for the next visit to the mechanic, but for car FBT (Fringe Benefits Tax) reporting on your business’ vehicles.

You’re providing a car and it’s your obligation to report to the tax office, but it’s your employees who are in the driver’s seat. They are responsible for maintaining a logbook to record their travel details – work-related and personal.

To make the most of tax savings, you’ll want an efficient method for preparing your car FBT report and how to make it easier for your employee to do the same.

And we all know, no one likes to do tax once, let alone twice.

Hassling your employees for their logbooks and expenses right at the end of the FBT year is likely going to be headache for both of you because it’ll be a mad rush to get everything in line.

Instead of leaving things to the last minute, make it easy for yourself and your employees to keep records across the year while being tax efficient.

Making the most out of the logbook

If using the operating cost method: a logbook is valid for 5 years so long as your employee doesn’t change their driving habits too much.

If the car changes driver and their driving habits are likely to be similar, then the logbook doesn’t need to be recorded again unless the 5 year period expires. Talk to your employee receiving the car about how they think they’ll use the car to make an informed judgement.

Once you provide someone with a car, put a logbook ready to go in their glove box and let them know it’s there. Also, link them to this article about logbooks so they’re informed.

Encourage them to complete the 12 week logging when business is most busy. That way, the more your employee is using the car for work purposes, the less car FBT you’re paying.

If your employee is more tech-inclined, you can also consider offering a digital app to avoid transcribing logbook details. However, test if the app is easy to use for your employee without bugs and provides accurate results you can download and work with, otherwise it’ll be as much, if not more, of a hassle than a traditional book.

There are certain technologies that can record all the details automatically. However, there are laws across Australia forbidding you from tracking their GPS data unless they give explicit consent. So double check that first.

Paper-less car expenses

Provide your employee a fuel card to use every time they make petrol or car-related expenses. Depending on the provider you choose, you can apply additional features like limit the services they can use the card for, such as specific petrol stations.

No receipt juggling!

Automate reminders

Send your employees reminders to give you their completed logbooks and expenses long before the lodgement time. At the start of the year is when people’s minds are fresh, which is a good time to give that first nudge.

Understanding car FBT for Companies

FBT is the tax that employers pay on certain benefits they provide to their employees or their employees’ associates that doesn’t involve salary.

The critical dates for reporting are:

- 31st March: end of FBT year. Collect all your details up to that point.

- 21st May: lodgement due date if you’re NOT lodging electronically or through a tax agent.

- 25th June: lodgement due date if you are.

Company cars are one of the most common fringe benefits targeted. The Australian Taxation Office (ATO) provides two ways you can report them.

The two vehicle tax reporting options

You have two paths to choose from:

- Operating Cost Method: calculates the actual running costs of the car and multiplies them by the percentage of private use. It requires more tracking, but like a finely tuned engine, it can be more tax-effective.

- Statutory Formula Method: applies a fixed percentage of 20% to the cost of the car, and factors in the amount of private use. Think of it as cruise control; less monitoring, but less tax-efficient.

What you need for Operating Cost

- A logbook maintained by an employee for 12 consecutive weeks, which details for every trip:

- The date travelled

- Odometer reading at the start of the trip

- Odometer reading at the end of the trip

- Number of kilometres travelled during each trip (calculated from the above)

- If the trip was work-related or private. Travelling from home to work and back is NOT classified as work-related.

- So long as the business pattern of use doesn’t change significantly, it’s valid for 5 years.

- Any contributions made for the car by the employee, not reimbursed by the employer (if applicable)

- you need to account of 1/11th of the amount as GST.

- it can include a declaration (in an approved format, backed up by receipts) for fuel, oil and other car-related expenses. These payments are inclusive of GST and not considered taxable.

- Expenses related to the vehicle:

- Registration

- Insurance

- Deemed depreciation and deemed interest (if the car is owned by your business)

- lease costs (if the car is leased from a third party)

Link your employee this article so they know what to keep track of.

To approximate how much tax you’d pay:

Taxable value = (Total operating costs x the % of private use based on log books) – employee contributions

This is more tax-efficient when employees use their cars regularly for work purposes, rather than private.

Fleets

If you own a fleet of at least 20 cars, you can use the simplified average: so long as valid log books are maintained for at least 75% of cars. With caveat: salary-sacrifice cars are excluded and the GST-inclusive cost of each car must be within the luxury car limit.

Depreciation

Cars acquired on or after 10 May 2006 have a deemed depreciation rate (diminishing value) of 25%.

What you need for Statutory Formula

- Cost of the motor vehicle, which includes:

- dealer delivery charges

- GST

- customs duty paid

- after 4 years owned or leased, the cost of the car is reduced by 1/3 at the start of the FBT year

- Excludes:

- Registration fees

- Stamp duty

- Extended warranty expenses

- The date it was purchased

- The number of days it was used for personal purposes. So if it hasn’t been provided the whole year, the taxable value is reduced accordingly.

- Any contributions made by the employee to the employer, not reimbursed (if applicable)

- you need to account of 1/11th of the amount as GST

- it can include a declaration (in an approved format, backed up by receipts) for fuel, oil and other car-related expenses. These payments are inclusive of GST and not considered taxable.

- this is more tax effective if the employee’s tax rate is lower than the current FBT rate, because it reduces the benefit’s value dollar-by-dollar

To approximate the tax payable using this method:

Taxable value = (Cost of the motor vehicle x Statutory Rate (20%) x No. of days of private use) ÷ 365 – employee contributions

In the past, this was a more popular option for calculating car FBT because it is straightforward and easy to track. But you could be paying more tax, regardless if the vehicle has only been sitting in your employee’s garage.

Which one is right for me?

As a rule of thumb, the Operating Cost method is best suited when you have a limited number of cars and therefore not too much chasing up to do with each employee. You may consider the Statutory Cost when the cost of keeping all your cars’ records up to date is more costly than the amount of tax you’d be paying.

Your choice will depend on your business scenario and resources available for tracking, and it’s best to consult your accountant on what’s the most tax effective for your situation.

What’s Exempt from car FBT?

Not all vehicles attract car FBT. Exemptions apply typically to vehicles designed to carry loads rather than passengers, like certain utes and panel vans, given they meet certain conditions and their private use is limited.

Electric vehicles

The laws for electric vehicles are constantly evolving as this new technology develops on a global basis. Make sure to keep an eye out on government updates, especially the yearly budget. See our latest FBT changes to look out for in 2024 for more details.

- Electric car vehicle exemptions only apply to employees specifically, not anyone else.

- Home charging stations

- It has to be a car, not something bigger like a van, or smaller like a motorbike

The rest of the FBT return

Got all the details for your car together and your employees were nice enough get back to you on time? Great! But you’re not done yet.

Sorry.

Remember that FBT applies to many benefits that don’t involve a salary, including their associates.

Non-salaried benefits such as:

- Low interest loans used for personal purposes

- Gym or health memberships

- Entertainment and recreational expenses (concert, cinema or other tickets, food, accommodation etc.) Additional rules apply, see below.

- Payment of personal expenses

- Private health insurance

- Shares or bonds

- Residential leases

There are also exemptions:

- on-premises recreational or child care facilities

- Portable electronic devices (e.g., laptop, ipad, printers, GPS, etc.) Larger businesses can only purchase or reimburse one portable electronic device for each employee per FBT year.

- A handbag, briefcase or satchel to carry items you need to use and carry for work. Such as for laptops, tablets, work papers or diaries. Be warned: if you are using these bags for a mix of personal and work use, then apportion the use, and it won’t be fully exempt from FBT. The ATO is not going to pay for your Gucci bag even if you throw your Ipad into it on occasion.

- Tools of the trade.

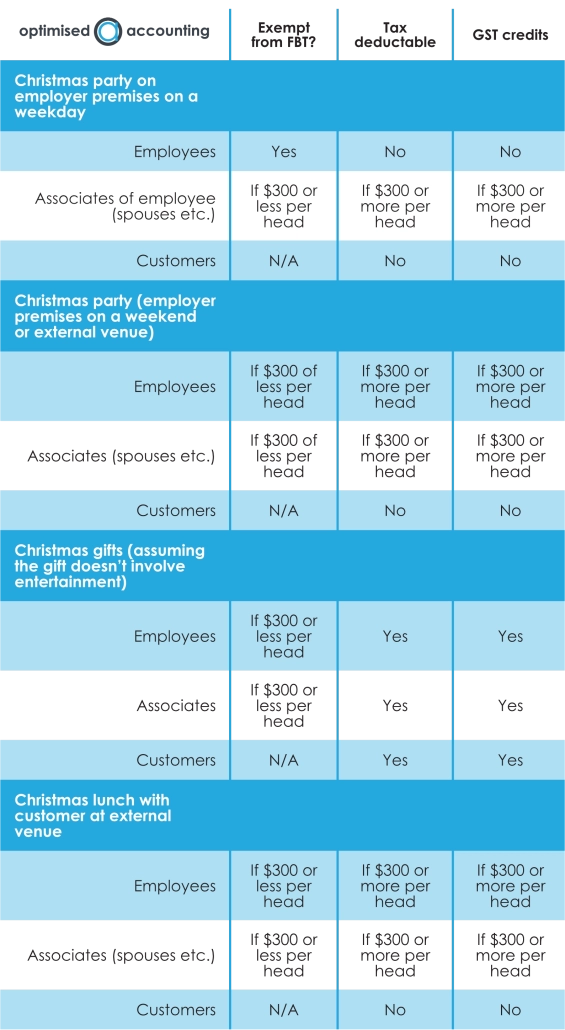

Gift deductions

As far as gifts of entertainment or non-entertainment value are concerned, you may be able to avoid FBT if you stick to certain limitations. In some cases, you can also claim the expenses as tax deductable or claim GST credits.

Let’s summarise:

The ATO can spot an issue when an employer pays for an expensive entertainment expense – meals out, tickets to footy matches etc – without a corresponding fringe benefit. Entertainment expenses aren’t usually tax deductible and you can’t claim GST credits unless the expenses are subject to FBT.

The $300 rule

If your business uses the ‘actual’ method for FBT and the benefits’ value is under $300, and on an infrequent and irregular basis, then there might not be any FBT implications.

If the business uses the 50/50 method, then 50% of the meal entertainment expenses would be subject to FBT. The minor benefits exemption would not apply. This means you can deduct half the expenses and the company can claim half of the GST credits.

You should keep records regardless if there’s nil taxable value involved, for example when an employee pays you contributions towards the benefit. Otherwise the ATO can revisit prior years at any time, rather than limited from 3-6 years.

Similarly, it’s also good practice to be registered for FBT once you have employees, even if you’re not yet providing any benefits and just submitting notices of non-lodgements.

Keeping the above in mind, FBT applies in general if the total taxable value in an FBT year exceeds $2000 and this must be reported on your employees income statement for that income year.

The lodgement process

You can lodge a few different ways:

- electronically using a Standard Business Reporting (SBR)-enabled software

- through a tax agent

- by post

Your Trusted Pit Crew

Are your wheels spinning yet? FBT is complex, and there are many more requirements and considerations which may apply if your business has more layers.

We at Optimised Accounting focus on simplifying your tax requirements by:

- Send you details on your FBT based on information you’ve provided us, so what you can focus on is confirming them rather than working them out from scratch

- Chase you up regularly to ensure you have everything ready to go come lodgement time

Once we cover those bases, we go beyond as business advisors for strategising your growth, so you and your team can spend more time driving to do what you’re best at doing.

Learn more tips for optimising your business

There are many tricks to the trade, and if you want to make the most of them to grow your business, jump into our email newsletter:

[activecampaign form=27 css=0]