Christmas is coming – avoid being stung by FBT

Don’t want to pay tax on Christmas? Here are our top tips to avoid giving the Australian Tax Office a bonus this festive season.

For most business owners, it’s time to start thinking about saying thanks to your employees for another year of hard work. It sounds great in theory: Christmas parties, client gifts, extra boons…

But it’s important to be aware of the tax implications of any gifts and celebrations you provide, or else the only one happy about the season will be the ATO.

Let’s see how we can avoid paying more tax in the form of FBT this Christmas time:

Firstly, what is FBT?

Fringe benefits tax is an additional tax that is imposed for giving staff a benefit aside from their salary/wage. This includes things like paying for a company car that is also available for personal use, providing a gym membership – and Christmas parties.

Please be aware that costs exempt from FBT generally cannot be claimed as tax deductions.

Keep it spontaneous with the $300 rule

$300 is the minor benefit threshold for FBT so anything at or above this level will mean that your Christmas generosity will result in a happy gift to the ATO at a rate of 47%.

Spending under $300, infrequently (so no monthly gym memberships), is classed as a ‘minor benefit’ and doesn’t attract FBT. Therefore, providing a meal and drinks under $300 per head at a restaurant will be considered a minor benefit, and will not attract FBT.

Cash gifts and Christmas bonuses are considered salary and wages. So PAYG withholding applies and the amount is normally subject to the superannuation guarantee. It’ll be considered ordinary time earnings unless it relates specifically to overtime work. Off the books doesn’t mean off the tax hook!

The Christmas Party Crunch

If you hold your Christmas party at your business premises on a work day, with current staff only – your Christmas party will be FBT free. In this scenario, there is not a limit of what you can spend per person. However, if family members of staff attend the function, the $300 limit per person applies for the non-staff attendees – otherwise an FBT liability may arise.

If you’re looking at celebrating out of the office be sure to stick to under $300 per person.

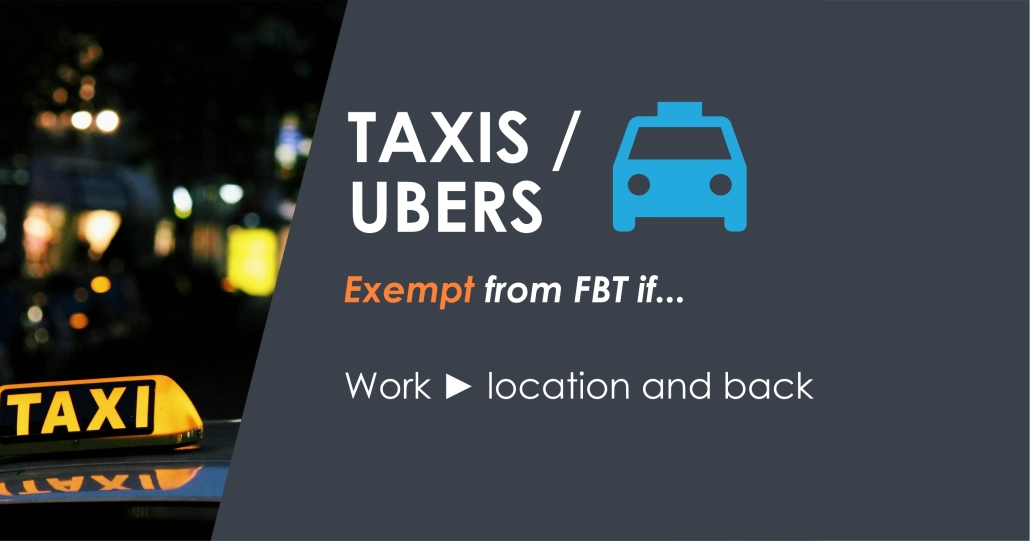

Going for a ride

If you have a few team members that need to be loaded into a taxi after overindulging in Christmas cheer, covering their ride is sure to be a relief across the board.

If the party takes place outside of work premises, the ride to the venue and back to work is generally FBT free. From your employee’s home to location and back may attract FBT.

This taxi travel is taken to be a separate benefit from the party itself and any Christmas gifts you have provided. This means that if the cost of each item per person is below $300, then the gift, party and taxi travel can potentially all be FBT free. Just remember that the minor benefits exemption considers a few factors, including the total value of associated benefits provided across the FBT year.

If your business hosts slightly more extravagant parties and goes above the $300 per person minor benefit limit, you will pay FBT but you can also claim a tax deduction and GST credits for the cost of the event. Just bear in mind that deductions are only useful to offset against tax. If your business is paying no or limited amounts of tax, a tax deduction is not going to help offset the cost of the party.

Business Christmas parties are classed as an extension of the work place – you are responsible for your employee’s safety, so it’s a good idea to cover these costs.

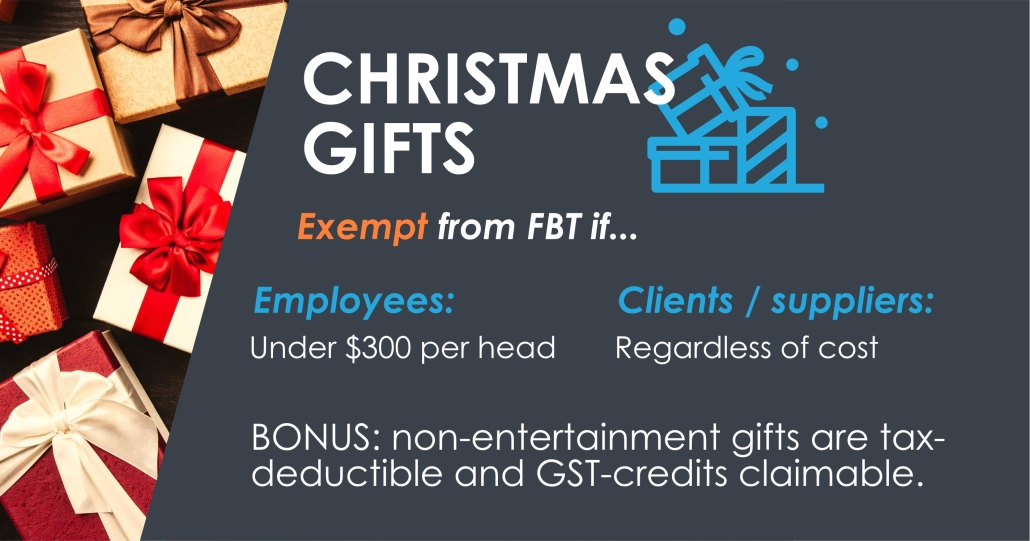

Gifts instead of lunches

The most effective way of sharing the Christmas joy with employees is not necessarily the most tax effective. If, for example, you take your employees out or entertain them in any way, it’s not tax deductible and you can’t claim back the GST. Restaurants or meals shared, theatre tickets, sightseeing tours, holidays, a show, golf, and corporate race days all fall into the ‘entertainment’ category.

Non-entertainment items, on the other hand, allow you to claim them. These can be things such as a bottle of wine, carton of beer, food hamper or grazing box, flowers, or even a box of chocolates.

Gifts to clients/suppliers

Gifts to clients or suppliers are similar to employees, in that you can’t claim entertainment as either deductions or GST claims. This is true regardless whether entertaining your clients results in more sales. And if you’re going for non-entertainment items, the same way, they are claimable so long as there’s an expectation your business will benefit.

Where the main difference is there’s no $300 cap where FBT is applied afterwards. So you could go hog if you believe it’s worth the investment.

You could also make a donation on behalf of your clients (where your business takes the tax deduction) or for your clients (where they receive the tax deduction).

Charities love cash

Charities love cash. They don’t have to spend any of their precious resources to receive it – unlike a lot of charity dinners, auctions, and promotional campaigns. And, from a tax perspective, it’s the safest way to ensure that you or your business can claim a deduction for the full amount of the donation.

There are a few rules to giving to charities that make the difference between whether you will or won’t receive a tax deduction.

The charity must be a deductible gift recipient (DGR). You can find the list of DGRs on the Australian Business Register (use the advanced search).

If you buy any form of merchandise for the ‘donation’ – biscuits, teddies, balls or you buy something at an auction – then it’s generally not deductible. Your donation needs to be a gift, not an exchange for something material. Buying a goat or funding a child’s education in the third world is generally ok because you are generally donating an amount equivalent to the cause rather than directly funding that thing.

The tax deduction for charitable giving over $2 goes to the person or entity who made the gift and whose name is on the receipt.

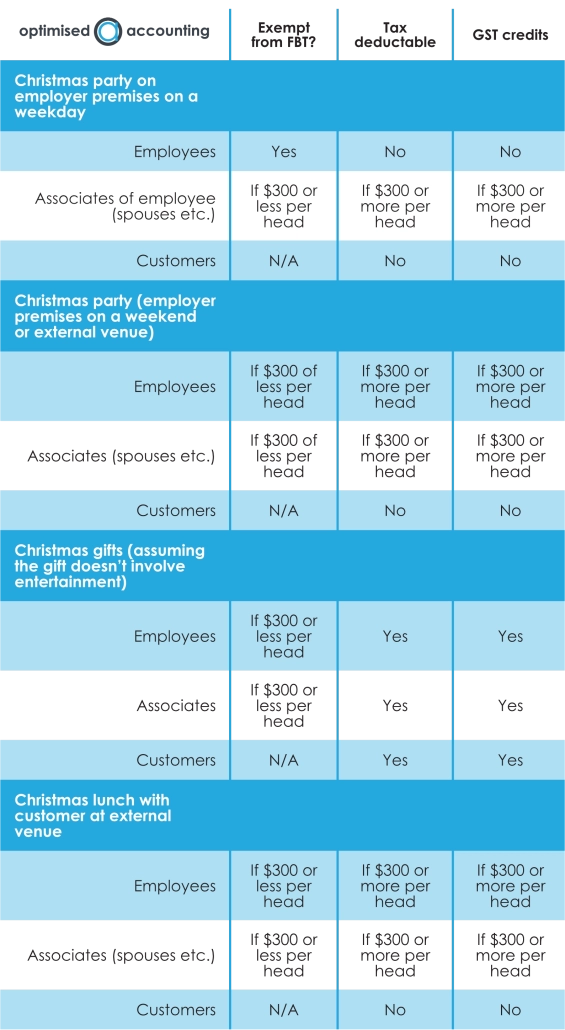

To summarise

Understandably there’s so many overlapping rules, it’s hard to balance between the optimal tax effective option and one which will reward your team.

So below is our cheat sheet of everything we’ve covered above. The information is for GST registered businesses that are not using the 50-50 split method for meal entertainment. You can download a printable version here.

Where to from here?

FBT returns are due in May, unless you have an accountant complete your return for you, in which case it’s due in June. So any FBT you need to pay for Christmas related expenses won’t need to be calculated until then.

If you’re a client with us, we will send you an FBT questionnaire closer to this time. We generally when preparing your BAS we ensure the GST treatment on entertainment is correct, however we rely upon you providing details about your Christmas party to us at FBT time.

For now, it’s a good idea to keep the $300 limit per person in mind when organising your Christmas parties and gifts for your staff – and one that can potentially save you a lot of money.

FBT is confusing at the best of times, and we are here to help if you have any questions. If you’d like a one-on-one discussion about your business, fill in your details here and we’ll organise a discovery meeting.

Happy organising!

Learn more tips for optimising your business

There are many tricks to the trade, and if you want to make the most of them to grow your business, jump into our email newsletter:

[activecampaign form=27 css=0]